2026 California 60 Hour Qualifying Education

Ready to become a California Registered Tax Preparer? This course gives you everything you need to meet the state's 60-hour qualifying education requirement — and start building a career with real earning potential. Approved by the California Tax Education Council, Vendor #2080, so you can enroll with confidence that it satisfies your CRTP requirement.

You'll work through 13 in-depth chapters covering federal and California tax law, then put your skills to the test with hands-on Practice Tax Returns (PTRs) after key chapters — so you're not just memorizing rules, you're learning to prepare real returns. When you're ready, you'll sit for three CTEC-required finals (Ethics, Federal Tax Law, and California Tax Law), all taken online at your own pace.

No classroom, no waiting for a session to start — enroll today and begin working toward your CRTP status right away.

📚 What is a Self-Study Course?

Take as long as you need. No deadlines, no rush — just progress on your schedule.

Enroll today and begin immediately. No waiting for a class to open or a session to start.

All materials are included. You study independently through readings, lessons, PTRs, and final exams.

What You'll Be Able to Do

- Determine a taxpayer's filing status and dependents

- Apply standard and itemized deductions

- Report income, capital gains, and self-employment earnings

- Prepare a complete federal Form 1040 and California Form 540

- Know your limited representation rights

- Apply for your IRS PTIN

- Register with CTEC as a CRTP

- Launch your career as a paid tax preparer

Course Chapters

Get familiar with the main individual federal and California tax return forms — their structure, sections, and how it all fits together.

Learn how to determine the right filing status, who qualifies as a dependent, and how to choose between standard and itemized deductions.

Understand all types of taxable income — wages, tips, interest, dividends, and more — and where they go on the return.

Discover above-the-line deductions like student loan interest and IRA contributions that can reduce taxable income.

Learn about additional taxes like self-employment tax and the penalties taxpayers may face for underpayment or late filing.

Explore how withholding, estimated payments, and valuable credits like the Child Tax Credit and EIC reduce what a taxpayer owes.

Dive into Schedule A deductions including mortgage interest, medical expenses, and charitable contributions.

Learn how to report profits and losses from selling stocks, real estate, and other assets — and how tax rates apply.

Understand how to deduct the cost of business assets over time using methods like Section 179 and bonus depreciation.

Used for self-employed individuals and sole proprietors to report business income and expenses on their personal return.

Covers supplemental income from rental properties, partnerships, S corporations, and trusts.

Learn how to file Form 4868 for an extension, correct a return with Form 1040-X, and navigate e-filing options.

Covers the professional standards and responsibilities tax preparers must follow, including Circular 230 guidelines and CRTP requirements.

Complete the Ethics, Federal Tax Law, and California Tax Law finals to earn your 60-hour QE certificate.

* Practice Tax Returns (PTRs) are completed after select chapters and include their own review questions based on material covered up to that point.

Course Details

| Detail | Info |

|---|---|

| Field of Study | Federal Tax Law — 43 hrsEthics — 2 hrsCalifornia Tax Law — 15 hrs |

| Total Hours | 60 Hours |

| Course Level | Basic |

| Prerequisite | None |

| Delivery Method | Self-Study |

| Expiration Date to Earn CEs | June 30, 2027 |

| Upon Completion | 🎓 Certificate of Completion |

| CTEC Vendor | #2080 |

| Course ID | 2080-QE-0001 |

* This course does not qualify for Federal CE hours.

Self Study

Learn at your own pace, read or watch the lessons, pass the exams.

Mobile Friendly

Learn on your phone, tablet, or computer.

Bilingual

All our courses are available in English y español.

Career Paths

No matter where you’re at in your career, we have courses for you.

Simple Learner Experiences

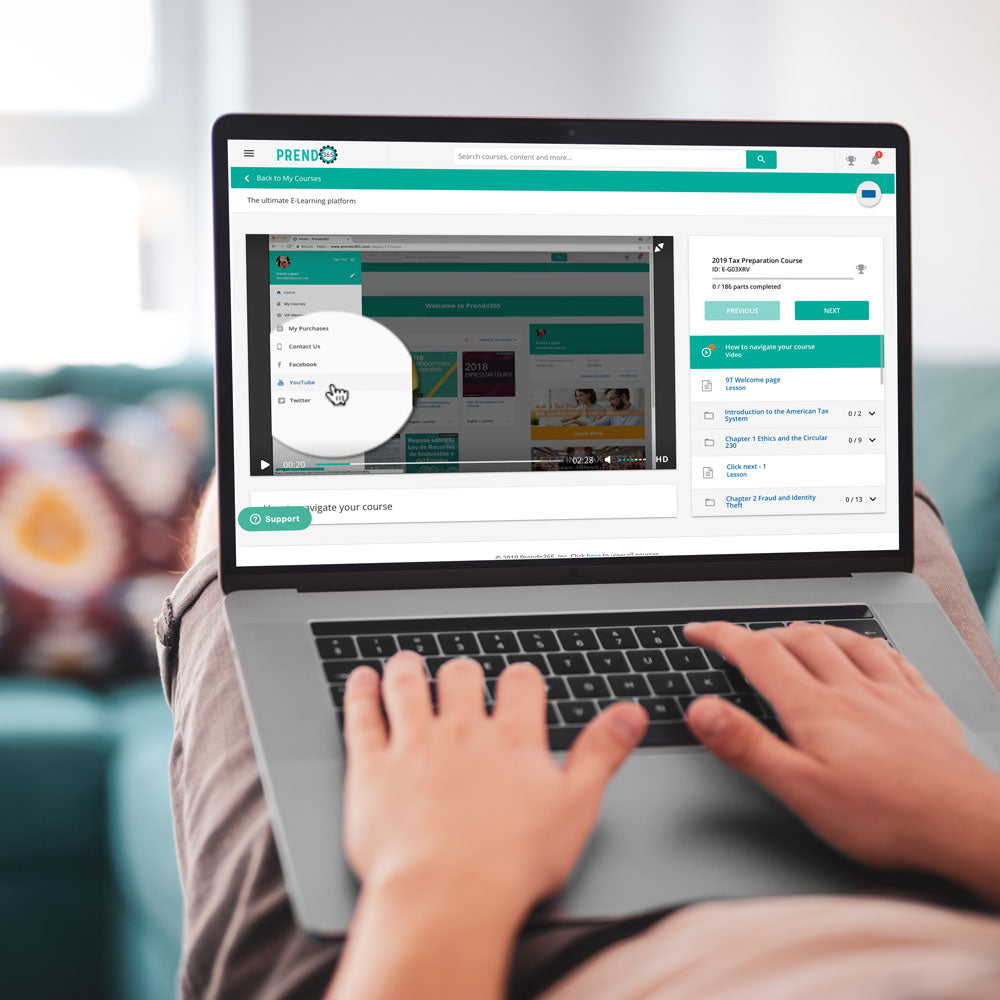

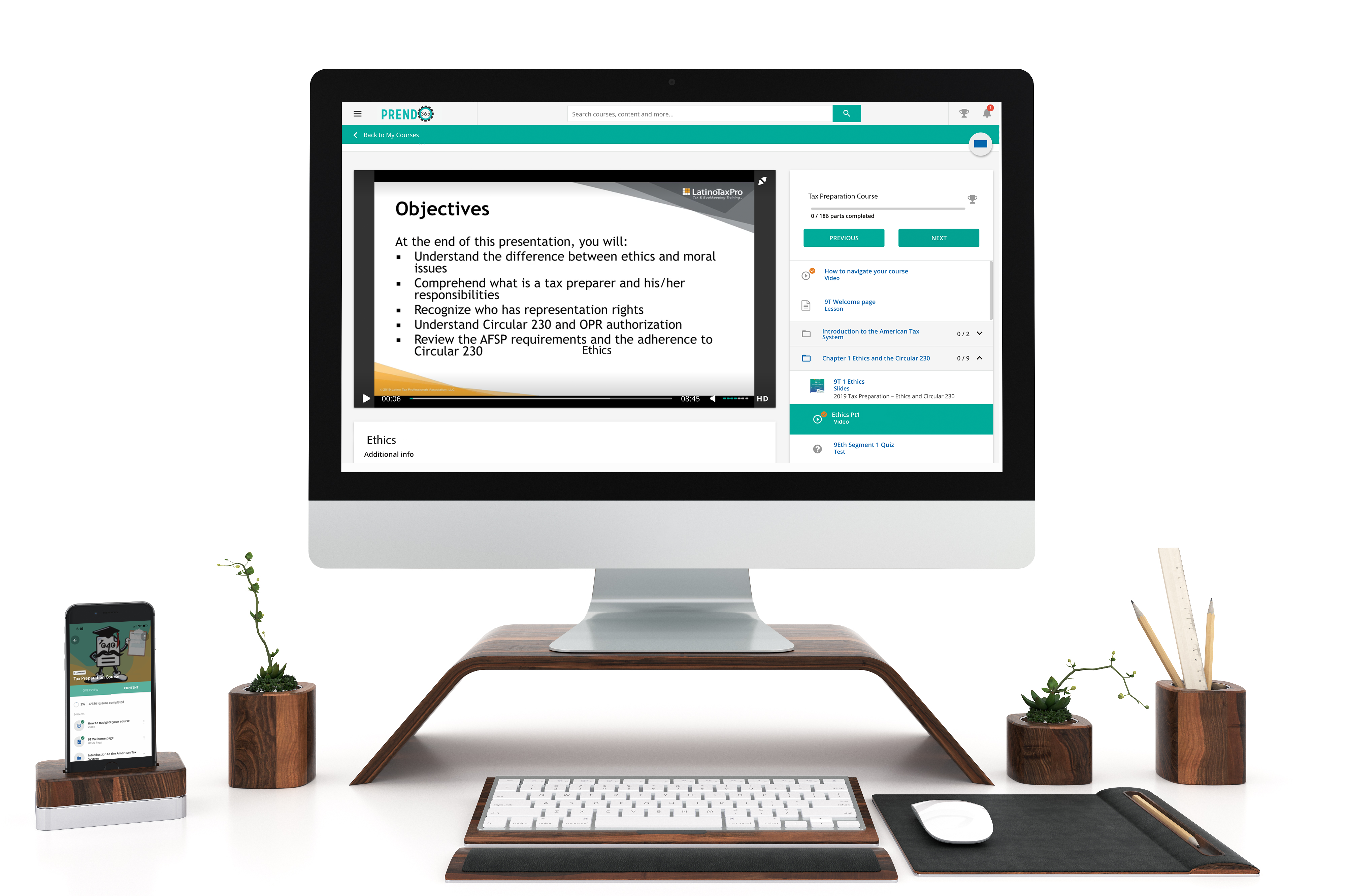

Prendo365 gives you access to your course anytime, anywhere, on desktop, tablet, or mobile device. You're able to easily navigate through your course and receive your certificate of completion.

Why choose us

Over 35+ years tax preparation experience

We know what tax preparers need to succeed in their office

7+ EA’s and tax preparers on staff

Our team does extensive research to ensure you receive the best education

Bilingual live support

Having technical issues? We're ready to help you get started and complete your course.